Across Europe, steelmakers face falling demand, global competition and the challenges of decarbonisation. Whilst Port Talbot will be switching to less energy-intensive electric arc furnaces, Sanjoy Sen looks at the alternative technologies that are emerging.

Steel isn’t big business, it’s massive business. But its losses can be equally huge.

Even in today’s high-tech, AI-enabled world, steel remains an economic cornerstone. McKinsey estimates it contributes €80 billion in direct value to the European economy, plus an added €1 trillion to the automotive, machinery and construction sectors. The employment stats are equally impressive: some 300,000 direct jobs plus over 2 million more in the supply chain and induced activities. Steel still matters.

Challenges abound

Right now, the industry finds itself in a period of major uncertainty. British and European steelmakers face a daunting combination of challenges: falling demand, fierce global competition and the challenges of decarbonisation.

Innovative. Informed. Independent.

Your support can help us make Wales better.

Little did I know it at the time, but my undergraduate stint at British Steel was to coincide with the company’s peak. Painful re-structuring had just seen major sites close: Corby (1979), Consett (1980), Shotton (1980), Ravenscraig (1992). But a competitive global player had emerged and by the early nineties, it was Europe’s number one. Soon afterwards, global supply began to ramp up, especially from China. Established competitors merged: British Steel and the Dutch giant Hoogovens formed Corus in 1999 and were later swallowed up by India’s Tata in a 2007 takeover.

The following year, the global economic crisis hit steel-hungry sectors, especially construction, hard. That knocked 35 million tonnes (almost 20%) off European demand and it hasn’t returned. More recently, Covid-19 has hit demand further. In response to overcapacity, plants have closed including British Steel’s former Redcar site.

Steel is responsible for 8% of global greenhouse gases and the industry is under pressure to take action.

Back in my day, no Chinese manufacturer was even in the global top 20. But by 2021, Chinese output exceeded a billion tonnes, more than the rest of the world combined and far exceeding the UK’s 7 million. And with falling Chinese domestic demand likely to create greater exports, the UK (and others) continue to rely on quotas and tariffs to stem the tide.

Meanwhile, the cost of tackling emissions has emerged as a major challenge to the sector. Steel is responsible for 8% of global greenhouse gases and the industry is under pressure to take action (Port Talbot came under the spotlight as the UK’s largest emitter). But this doesn’t come cheap: the global cost of steel decarbonisation is estimated at an eye-watering £4.4 trillion.

Government options

That leaves governments with some tough choices, from allowing market forces to potentially wipe out domestic producers through to nationalisation and taking on the industry’s problems. The UK is not alone in facing these challenges: Nippon Steel’s proposed $15 billion takeover of struggling US Steel looks set to be blocked with national security issues playing out ahead of the presidential election.

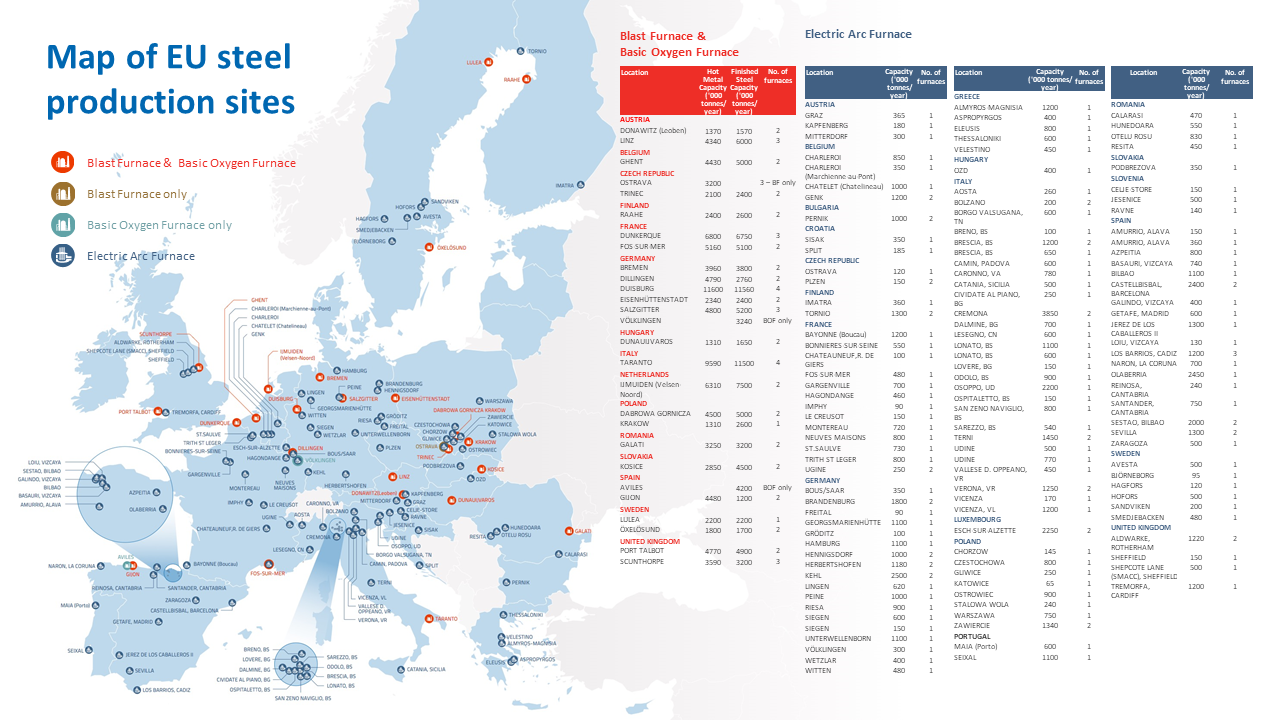

Post-Brexit, the UK government has opted to keep foreign owners afloat and sees the electric arc furnace (EAF) as the answer. EAFs use electricity (and lots of it) to produce steel from scrap at lower cost (and a quarter of the emissions) than traditional blast furnaces fed by raw materials (iron ore, coal).

That leaves governments with some tough choices, from allowing market forces to potentially wipe out domestic producers through to nationalisation and taking on the industry’s problems.

Tata secured £500 million in UK Government support to replace Port Talbot’s two blast furnaces with an EAF. And British Steel (now owned by China’s Jingye Group) is seeking £600 million for Scunthorpe and Teesside EAFs.

But as EAF’s share of world capacity approaches 50%, global scrap supply looks set to tighten, driving costs up. And whilst EAF capabilities are improving, ditching blast furnaces threatens to leave the UK rare amongst developed nations in being unable to produce higher quality, virgin steels. Worse still, the UK steel is burdened by high electricity costs, almost £100 per megawatt hour versus Germany’s £60, threatening the viability of EAFs.

Technology alternatives

EAFs are already operating in the UK (including at Celsa’s Cardiff site) and are catching on across Europe, too. But on the continent, governments are also dishing out state aid in pursuit of cleaner virgin steel routes. The front-runner here is DRI (Direct-Reduced Iron) which uses ‘green’ hydrogen generated from renewable power instead of coal-based coke. Earlier this year, Tata secured €3 billion from the Dutch government to bring DRI to the giant IJmuiden plant.

Robust debate and agenda-setting research.

Support Wales’ leading independent think tank.

In Sweden, blueprints for future integration and synergies are emerging. Steelmaker SSAB (not SAAB), mining firm LKAB and energy company Vattenfall have jointly created the HyBRIT DRI process. Stegra is also working on DRI having emerged as a spin-off from the Northvolt battery producer. Both have benefitted from government support. Whilst manufacturers accept their green steel will carry a cost premium, the incremental impact on the price of an electric car is estimated as small.

DRI is no silver bullet, however. It too has feedstock challenges. And although German steelmakers have enjoyed generous subsidies, Thyssenkrupp is getting cold feet as projected costs rise.

Managing the transition

With Port Talbot losses reportedly running at a million pounds a day, change was clearly essential. But following the rejection of a phased transition, the immediate closure of its two blast furnaces saw 2,000 jobs lost, potentially creating significant socio-economic impacts in the immediate area as well as having knock-on effects on the whole region.

These are momentous times for British industry. In the same week that Port Talbot’s blast furnaces fell cold, the last coal-fired power station also breathed its last.

Over in France, by contrast, ArcelorMittal will progressively replace its Dunkirk and Fos blast furnaces by 2030 with a combination of DRI and EAFs, supported by €850 million of government funding.

These are momentous times for British industry. In the same week that Port Talbot’s blast furnaces fell cold, the last coal-fired power station also breathed its last. At the same time, the UK government pledged £22 billion for low emission hydrogen production backed up by carbon capture and storage (CCUS); had these projects come forward earlier, they might have supplied new DRI plants at British steelworks.

There is much left to do. Other energy-intensive sectors (e.g. cement) also need to decarbonize. And emerging sectors (e.g. AI data centres) have growing power demands. Our industrial strategy needs to be on the front foot to tackle these challenges.

All articles published on the welsh agenda are subject to IWA’s disclaimer. If you want to support our work tackling Wales’ key challenges, consider becoming a member.

{kind=link}